Press & media kit

Everything journalists, bloggers, and researchers need to quote or cite Snowballr. Free to use with attribution. Please link to snowballr.io.

Press, interview requests, or fact-checking: /contact. Typical response time: 24–48 hours. Available for written quotes, on-the-record commentary, and data verification.

About Snowballr (short)

Snowballr is an independent personal-finance calculator publisher (snowballr.io). It builds free, no-sign-up calculators and original research on compound interest, debt payoff, retirement planning, and FIRE. All calculations run client-side; the site does not collect personal financial data.

Founder bio

Alex Malinescu is the founder and editorial director of Snowballr. He built the site after finding that most online compound interest calculators produce conflicting answers due to undocumented assumptions about compounding frequency, contribution timing, and inflation adjustment. Snowballr documents every formula and assumption directly on the calculator page.

Quick facts

| Founded | 2024 |

| Editorial team | Snowballr Editorial Team |

| Audience | US (primary), EU (ES/DE/PT) |

| Calculator coverage | 100+ free calculators in 4 languages |

| Original research | Datasets, schema.org Dataset-published, CC-BY 4.0 |

| Domain | snowballr.io |

| Hosting | Vercel (US edge) |

| License (research/API) | Creative Commons CC-BY 4.0 |

Quotable stats (use freely with attribution)

Each stat below has a primary source linked. Verify before publishing — and please cite Snowballr as the calculator/research source.

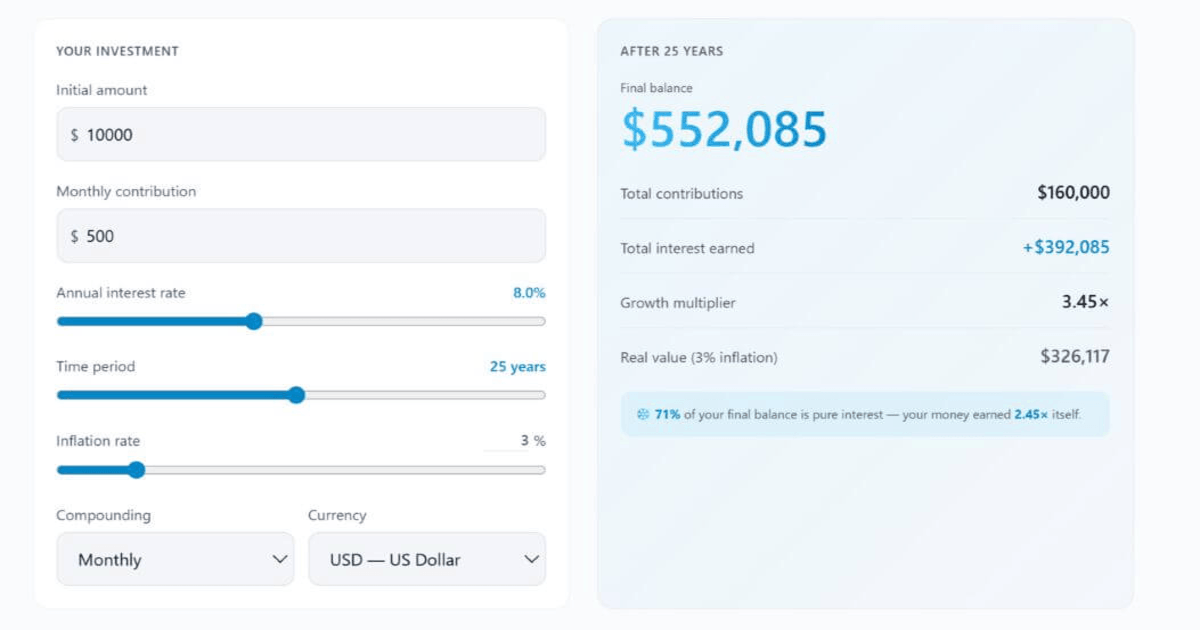

- “$500/month invested at 7% becomes $611,729 in 30 years.”Snowballr Compound Interest Calculator (snowballr.io/compound-interest-calculator)

- “A 5-year delay starting at age 25 vs 30 costs roughly 41% of your final retirement balance, all else equal.”Snowballr Cost of Waiting study (snowballr.io/cost-of-waiting-to-invest)

- “The S&P 500 returned 10.7% annualized over the past 30 years (1995–2024, dividends reinvested).”Snowballr Fast Facts hub, citing NYU Stern (snowballr.io/fast-facts)

- “A 1.0% expense ratio costs a typical investor $156K over 30 years vs a 0.05% index fund — at $500/mo contributions.”Snowballr Expense Ratio study (snowballr.io/research/expense-ratio-impact)

- “The avalanche debt method saves an average of 8% more interest than snowball — but ~70% of users finish snowball.”Snowballr Debt Snowball Comparison (snowballr.io/debt-snowball-vs-avalanche)

- “Of 5,000 Monte Carlo scenarios, investing rather than prepaying a 6.5% mortgage wins ~62% of the time over 15 years.”Snowballr Mortgage Prepay vs Invest study (snowballr.io/research/mortgage-prepay-vs-invest-5000-scenarios)

Topics Snowballr can comment on

- Compound interest math and common misconceptions

- Debt payoff strategy (snowball vs avalanche, math vs behavior)

- FIRE movement and 4% rule (Trinity, Bengen, post-2020 reassessment)

- Index fund fees and the long-run cost of high expense ratios

- Mortgage prepay vs invest the difference (with Monte Carlo)

- Roth vs Traditional IRA (break-even tax-bracket analysis)

- Emergency fund sizing across household types

- Student loan refinance vs forgiveness decision-making

- Inflation and real (vs nominal) returns

Brand assets

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Citation format

For research, please cite as:

Snowballr Editorial Team. "[Title of page]." Snowballr, 2026.

URL: [exact page URL]. Accessed [date].For shorter contexts (news, blog), via Snowballr with a backlink is fine.

Useful pages for journalists

- Fast Facts — canonical numbers with primary sources

- Data hub — published datasets

- How to cite Snowballr

- About — editorial standards, fact-checking

- Calculator API — verify any number programmatically

- Disclaimer — what Snowballr is and is not

This page last updated 2026. Brand assets and stats CC-BY 4.0.